Common Factors Used in FICO® Scores

A credit score is a number calculated from information in your credit reports. It is designed to help lenders estimate how likely you are to repay borrowed money as agreed.

Many commonly used credit scores range from 300 to 850, although different scoring companies and score versions may use different ranges. In general, a higher score may make it easier to qualify for credit and may help you receive more favorable interest rates and terms. A lower score may make approval more difficult or result in higher borrowing costs.

Your credit score is only one part of a lender’s decision. Income, debt, employment history, the type of credit requested, and other underwriting requirements may also be considered. Maintaining a stronger credit profile may help reduce the amount you pay in interest over the life of a mortgage, auto loan, credit card, or other credit account.

Many commonly used credit scores range from 300 to 850, although different scoring companies and score versions may use different ranges. In general, a higher score may make it easier to qualify for credit and may help you receive more favorable interest rates and terms. A lower score may make approval more difficult or result in higher borrowing costs.

Your credit score is only one part of a lender’s decision. Income, debt, employment history, the type of credit requested, and other underwriting requirements may also be considered. Maintaining a stronger credit profile may help reduce the amount you pay in interest over the life of a mortgage, auto loan, credit card, or other credit account.

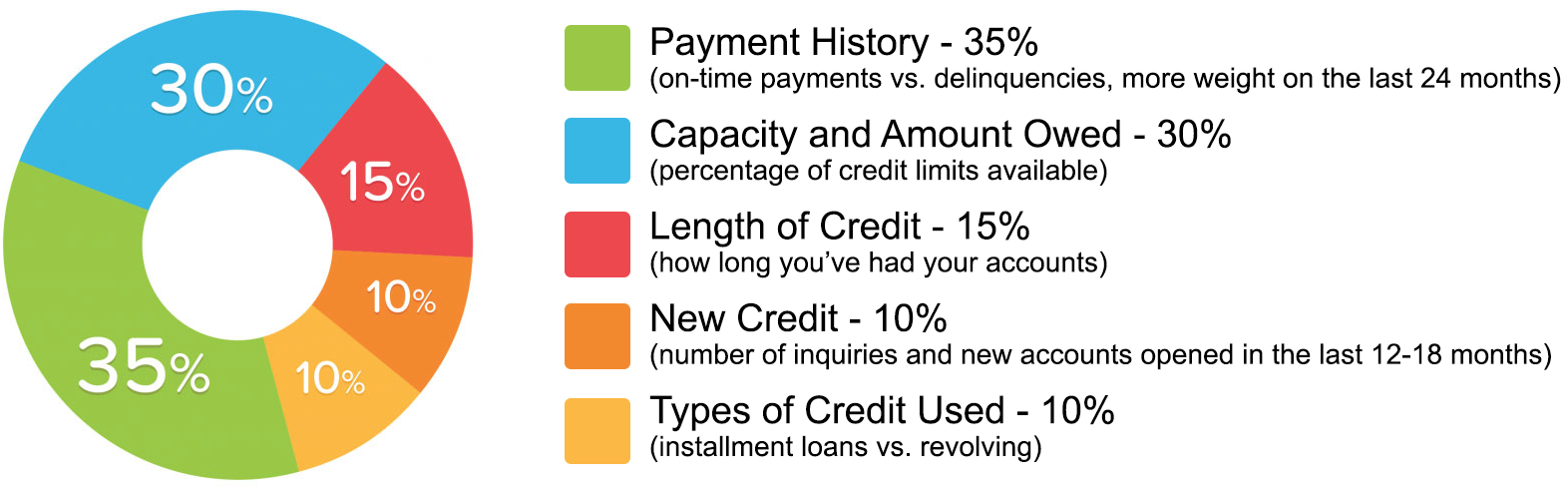

What affects your Credit Score?

This chart is provided for general educational purposes and reflects commonly cited FICO® scoring categories. The importance of each factor may vary depending on the scoring model used and the information contained in an individual consumer’s credit profile. Consumers may have multiple credit scores, and lenders may use different scoring models when evaluating an application.

Review Your Credit Reports for Accuracy

Next Chance Credit Consulting helps consumers understand the information appearing on their credit reports, including payment history, reported balances, credit utilization, inquiries, collections, account history, and other credit factors.

Depending on the service selected, NCCC may help identify information the consumer believes may be inaccurate, incomplete, duplicated, outdated, unverifiable, unfamiliar, or associated with another person.

Consumers have the right to dispute inaccurate or incomplete information directly with the consumer reporting agencies and the company that reported the information at no cost.

Accurate, current, and verifiable negative information generally cannot be removed merely because it is unfavorable. Next Chance Credit Consulting does not guarantee credit-score increases, account deletions, loan approvals, interest rates, or specific outcomes.

Depending on the service selected, NCCC may help identify information the consumer believes may be inaccurate, incomplete, duplicated, outdated, unverifiable, unfamiliar, or associated with another person.

Consumers have the right to dispute inaccurate or incomplete information directly with the consumer reporting agencies and the company that reported the information at no cost.

Accurate, current, and verifiable negative information generally cannot be removed merely because it is unfavorable. Next Chance Credit Consulting does not guarantee credit-score increases, account deletions, loan approvals, interest rates, or specific outcomes.

HOW LONG MAY INFORMATION REMAIN ON A CREDIT REPORT?

Credit-reporting time periods vary according to the type of information reported.

The following are general educational guidelines and may not apply in every circumstance.

Late Payments and Delinquencies

Late payments and other negative account-history information may generally remain on a credit report for up to seven years.

Collection Accounts

A collection account may generally remain for approximately seven years from the delinquency that immediately preceded the collection activity.

Paying a collection may update the account to show a zero balance or paid status, but payment does not necessarily require the account to be removed immediately.

Charge-Off Accounts

A charge-off may generally remain for approximately seven years from the delinquency that immediately preceded the charge-off.

The reporting period generally does not restart simply because the account is sold, transferred to another company, or later paid.

Closed Accounts

Closing an account does not automatically remove it from a credit report.

A closed account with negative history may generally remain for up to seven years. Positive account history may remain longer and can continue to contribute to the consumer’s credit history while it is reported.

Bankruptcy

Bankruptcy information may remain on a credit report for up to ten years. The length of time actually reported may vary according to the type of bankruptcy and the policies of the consumer reporting agency.

Civil Lawsuits and Judgments

Information concerning a civil lawsuit or judgment may be reported for seven years or until the applicable statute of limitations expires, whichever period is longer.

Public-record reporting practices may vary among consumer reporting agencies.

Tax Liens

Tax-lien information is governed by federal reporting requirements and the current policies of the consumer reporting agencies. Consumers should review their reports to determine whether a tax lien is actually being reported and whether the information is accurate and current.

Credit Inquiries

Hard inquiries may generally remain visible on a credit report for up to two years. Their effect on a credit score, if any, may be shorter and depends on the scoring model.

Soft inquiries, such as certain account reviews, pre-screened offers, and a consumer checking their own report, generally do not affect credit scores and are usually visible only to the consumer.

Medical Debt and Medical Information

Medical debt and medical information are subject to special federal rules and consumer reporting agency policies. Consumers should carefully review any medical collection appearing on a credit report for accuracy, status, balance, and eligibility to be reported.

The following are general educational guidelines and may not apply in every circumstance.

Late Payments and Delinquencies

Late payments and other negative account-history information may generally remain on a credit report for up to seven years.

Collection Accounts

A collection account may generally remain for approximately seven years from the delinquency that immediately preceded the collection activity.

Paying a collection may update the account to show a zero balance or paid status, but payment does not necessarily require the account to be removed immediately.

Charge-Off Accounts

A charge-off may generally remain for approximately seven years from the delinquency that immediately preceded the charge-off.

The reporting period generally does not restart simply because the account is sold, transferred to another company, or later paid.

Closed Accounts

Closing an account does not automatically remove it from a credit report.

A closed account with negative history may generally remain for up to seven years. Positive account history may remain longer and can continue to contribute to the consumer’s credit history while it is reported.

Bankruptcy

Bankruptcy information may remain on a credit report for up to ten years. The length of time actually reported may vary according to the type of bankruptcy and the policies of the consumer reporting agency.

Civil Lawsuits and Judgments

Information concerning a civil lawsuit or judgment may be reported for seven years or until the applicable statute of limitations expires, whichever period is longer.

Public-record reporting practices may vary among consumer reporting agencies.

Tax Liens

Tax-lien information is governed by federal reporting requirements and the current policies of the consumer reporting agencies. Consumers should review their reports to determine whether a tax lien is actually being reported and whether the information is accurate and current.

Credit Inquiries

Hard inquiries may generally remain visible on a credit report for up to two years. Their effect on a credit score, if any, may be shorter and depends on the scoring model.

Soft inquiries, such as certain account reviews, pre-screened offers, and a consumer checking their own report, generally do not affect credit scores and are usually visible only to the consumer.

Medical Debt and Medical Information

Medical debt and medical information are subject to special federal rules and consumer reporting agency policies. Consumers should carefully review any medical collection appearing on a credit report for accuracy, status, balance, and eligibility to be reported.

IMPORTANT INFORMATION ABOUT REPORTING PERIODS:

The expiration of a credit-reporting period does not necessarily mean that the underlying debt no longer exists or can no longer be collected.

The time allowed for information to appear on a credit report is different from the statute of limitations for filing a lawsuit to collect a debt.

Certain federal exceptions may permit older information to be reported in connection with some high-value credit, life-insurance, or employment-related reports.

Consumers should dispute information they believe is inaccurate, incomplete, duplicated, outdated, unverifiable, or not associated with them.

Accurate negative information generally cannot be removed merely because it is unfavorable.

Next Chance Credit Consulting provides general credit education and does not provide legal advice or guarantee the removal of information from a consumer’s credit reports.

The time allowed for information to appear on a credit report is different from the statute of limitations for filing a lawsuit to collect a debt.

Certain federal exceptions may permit older information to be reported in connection with some high-value credit, life-insurance, or employment-related reports.

Consumers should dispute information they believe is inaccurate, incomplete, duplicated, outdated, unverifiable, or not associated with them.

Accurate negative information generally cannot be removed merely because it is unfavorable.

Next Chance Credit Consulting provides general credit education and does not provide legal advice or guarantee the removal of information from a consumer’s credit reports.